How CBRS PAL Auctions Are Revolutionizing Wireless Infrastructure (And Why It Matters)

The wireless industry has long felt stuck in a mature, commoditized rut—flat ARPU, saturated consumer markets, and 5G hype that delivered faster Netflix but not the revolutionary new revenue streams everyone expected. But beneath the surface, a quiet revolution in spectrum licensing is reshaping how capital flows, networks deploy, and innovation happens. At the center of it is the Citizens Broadband Radio Service (CBRS) and its Priority Access License (PAL) auction framework.

The core innovation? Unbundling spectrum rights at a hyper-local level. It’s the spectrum equivalent of finally being able to buy just the one cable channel you actually want—without subsidizing 99 others you’ll never watch.

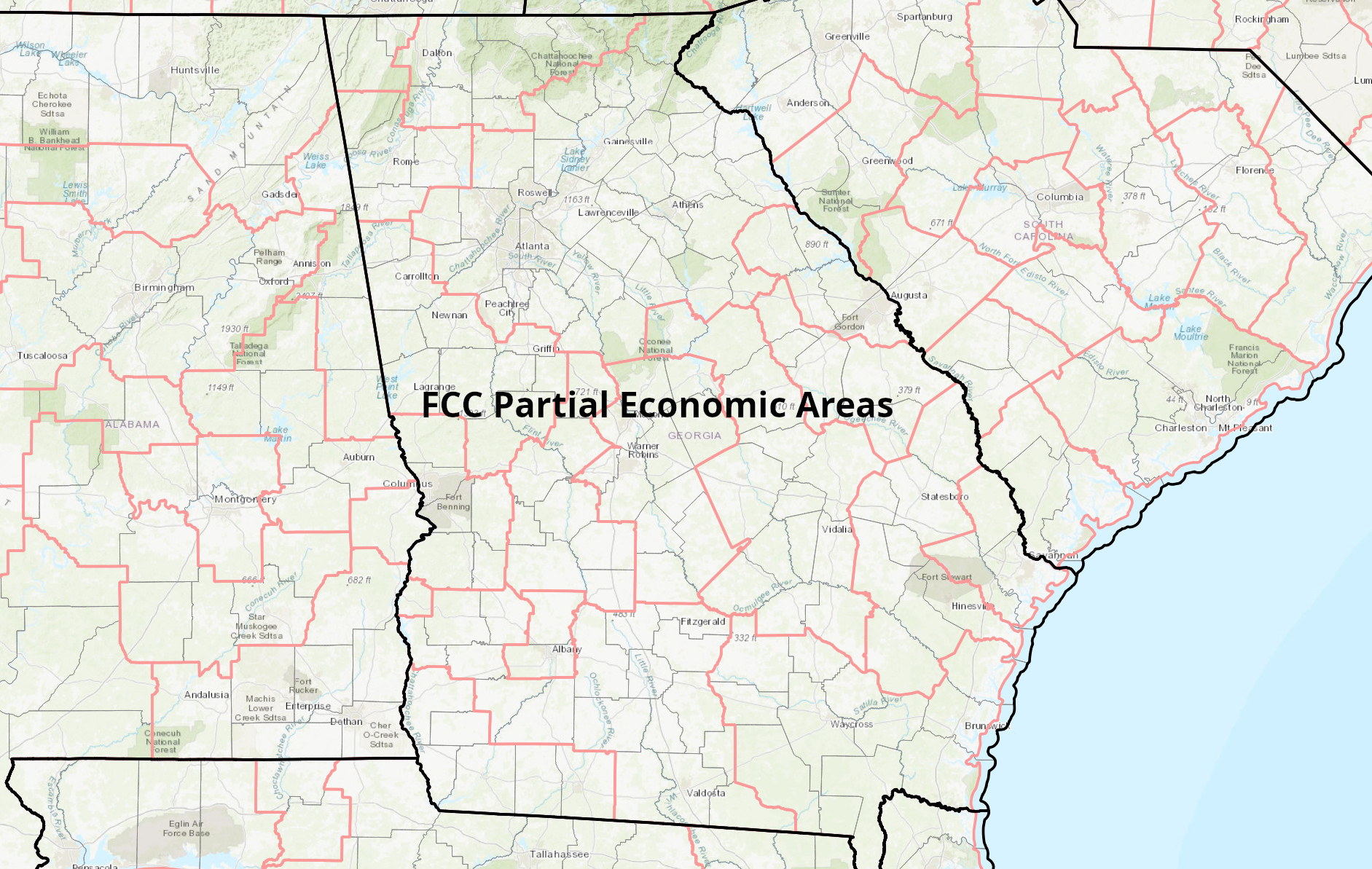

Traditional spectrum auctions often force bidders into large geographic bundles—Partial Economic Areas (PEAs), Cellular Market Areas (CMAs), or even nationwide licenses. If you want prime urban spectrum, you’re often stuck overpaying for vast rural footprints with marginal ROI. Capital gets misallocated: money pours into low-yield areas just to secure the high-value ones, or bidders sit out entirely. Price discovery suffers because bids reflect bundled economics rather than true market-by-market demand.

Result? Spectrum sits underutilized in places where it could drive real value, while high-potential markets get starved of focused investment.

The FCC’s 2020 Auction 105 for CBRS PALs flipped the script. Here’s how it worked:

Bidders could surgically target high-economic-yield counties (dense urban/suburban markets with strong enterprise, FWA, or industrial demand) without wasting capital on the rest of the country. The remaining spectrum everywhere stayed open for GAA—democratizing access for private networks, neutral hosts, utilities, and innovative deployments.

This unbundling delivered two powerful efficiencies:

It’s the opposite of cable bundling: targeted investment unlocks broader ecosystem value.

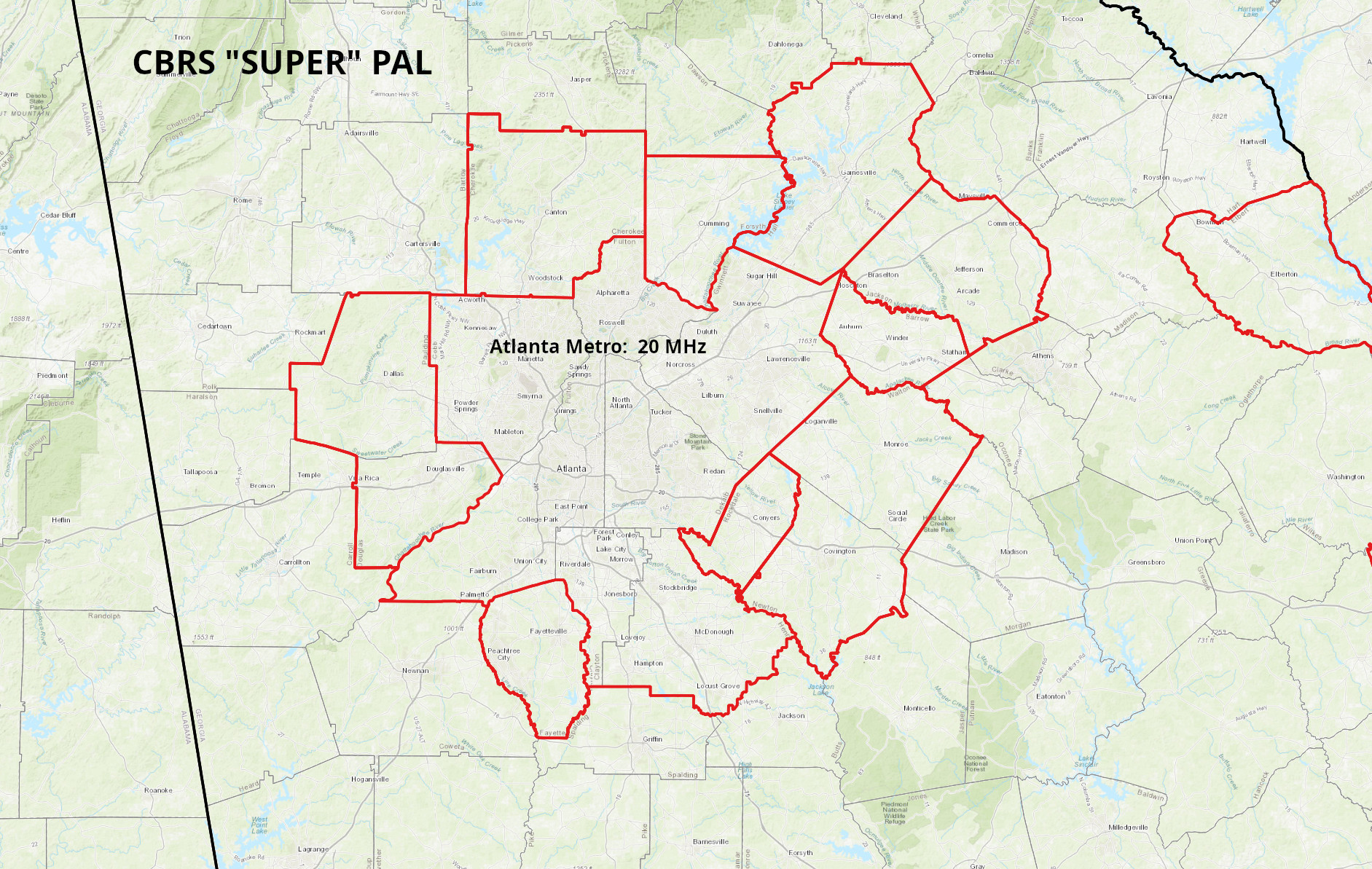

Nowhere is this unbundling playing out more elegantly than in the Atlanta, Georgia metro area.

One innovative PAL licensee swept up licenses across the entire 14-county Atlanta metro region. Rather than treating each county in isolation, they strategically consolidated holdings to engineer a virtual "super PAL”:

This isn’t just clever spectrum math—it’s a masterclass in market-driven efficiency. By focusing capital on Atlanta’s economic engine (logistics hubs, manufacturing, ports-adjacent activity, enterprise campuses), the licensee created a scalable, high-performance private wireless layer without overextending into low-density areas. The rest of Georgia (and the country) remains fully available for GAA users, system integrators, and smaller players.

The outcome? More spectrum effectively "in play” for real-world use, faster ROI on deployments, and a model that other markets can replicate. It demonstrates how county-level granularity + consolidation powers create exactly the right-sized network footprints for modern use cases: private 5G in factories/ports, FWA replacing cable broadband, and mission-critical enterprise connectivity.

This CBRS model isn’t just smart auction design—it’s foundational for the macro shifts we’ve been tracking in telecom:

The broader lesson: Spectrum policy that embraces unbundling, sharing, and localism accelerates deployment, spurs competition, and frees up capital for innovation. It moves us from "who owns the biggest pipe” to "who can make the smartest, most targeted use of spectrum.”

Traditional carriers still dominate consumer wireless, but the real growth—and the real differentiation—is happening in these localized, software-defined, enterprise-driven networks. CBRS PALs didn’t just auction spectrum; they unlocked a new architecture for wireless infrastructure.

We’re excited to be a part of this quiet revolution slowly working its way through the wireless industry.

Pages